First-time home buyer: Are you financially ready?

For most Singaporeans, moving out and buying their very first home is a huge milestone that usually goes hand-in-hand with getting married - either that, or turning 35 and ready to get your own space.

But between the excitement of browsing interior design ideas and listening to well-meaning relatives’ feng shui advice, it is important to think carefully about the finances involved in buying a home.

Since your new home is likely the most expensive purchase in your life so far, it can be difficult to budget for. But the last thing you want in this exciting new chapter of your life is to be blindsided by unexpected costs.

In this article, let’s tally up the potential costs of buying your first home so you can be prepared for what it’ll take.

Key Factors to Consider

It goes without saying the cost of your home is greatly dependent on property type. Depending on whether it’s an HDB BTO, HDB resale, executive condominium, private condominiums or landed houses, your home can cost anything from S$300,000 to S$3 million.

Other factors that impact home prices are location, amenities, remaining lease, and - importantly - the availability of housing grants.

If you haven’t the faintest idea about which property types are within reach, use the MyHome planning tool to calculate your maximum loan amount and work out an appropriate budget. You can also check your eligibility status for various HDB types.

Once you have decided on a property type and price range, it’s time to move on to the practical monetary considerations. It comes down to a few factors:

|

Immediate costs |

|

|

Future costs |

|

These factors are all interlinked, but a good way to think about it is in terms of the immediate costs (down payment, which depends on your home loan) and future costs (monthly repayments and loan period).

1) Immediate costs: Estimating your down payment

For many first-time home buyers in Singapore, the down payment is the single biggest financial concern.

The down payment typically needs to be paid at the point of official purchase. Depending on the home buying process (which varies with housing type), the down payment is due about 1 to 4 months from exercising the option to purchase.

And yes, that’s the case even for HDB BTOs and condos under construction - the down payment is due before your home is even in existence.

Depending on whether you take an HDB loan or a bank loan, the minimum down payment can vary quite a bit. For starters, the down payment is 20% with a HDB loan, and 25% with a bank loan. Furthermore, there are variations on whether you can pay this by cash or CPF.

Let’s take a S$500,000 HDB flat as an example.

If you already have your heart set on a particular property and know its price, you can use the MyHome planning tool to quickly determine the down payment needed for your dream home.

Alternatively, if you have some money saved up for the down payment, but have not picked a home yet, you can use it to find out what property price range you should be looking at.

2) Future costs: Servicing your home loan

The other part of the home loan equation is, of course, the mortgage, which will impact your life (for decades, in some cases!).

Unlike the minimum down payment, which is quite simple to calculate, the monthly repayment on your mortgage is a more complex affair. It largely depends on the loan amount and loan tenure you choose.

For example, a couple buying a S$500,000 HDB flat, opting for a 25-year bank loan, can expect to pay about S$1,572 to S$1,683 a month. (If they are Singaporean, this amount can come from their CPF Ordinary Account, regardless of property type.)

If they decide to shorten the loan tenure to 15 years, the monthly repayment shoots up S$2,396 to S$2,501. This makes them almost S$1,000 “poorer” (in terms of cash) every month, which may leave them cash-strapped during emergencies or unexpected expenses.

Pro-tip: You save more money by taking the maximum loan period you can. Even if you need to ’pay down’ your loan quickly, making a partial repayment saves your more money compared to taking a shorter loan tenure.

Bear in mind also that the government has rules, known as Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR), to prevent borrowers from committing to monthly repayments that are higher than they can actually handle.

It all sounds rather complicated, but you can cut out the guesswork by using the MyHome planning tool. This tool calculates your monthly instalments while taking your loan type, loan tenure, MSR and TDSR into account.

It’s Not Over Yet! Other Costs to Budget for

You’ve considered the down payment and monthly recurring loan payments – that’s a good first step! But don’t forget that you have a life outside of buying a home, too.

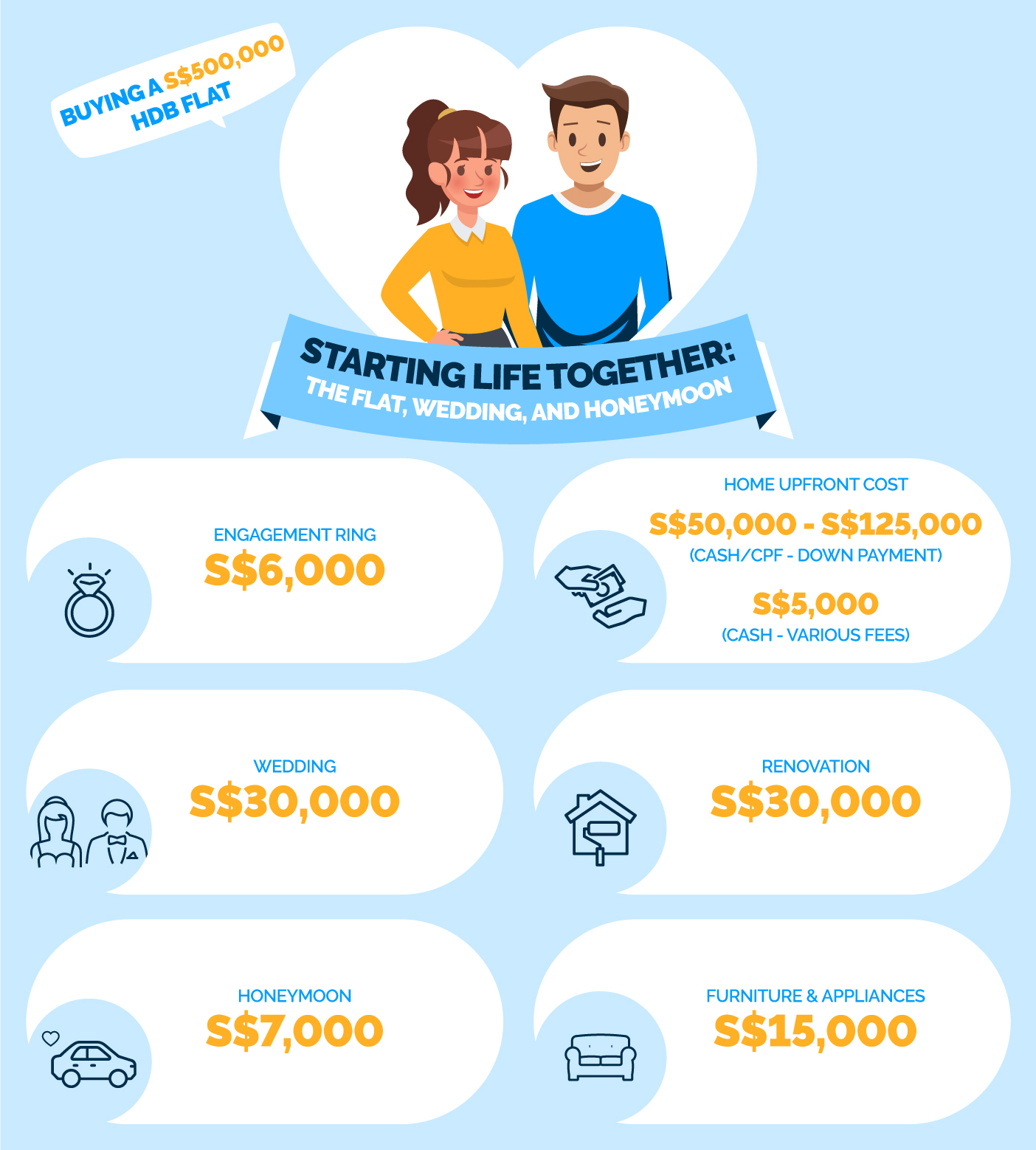

For couples who are about to tie the knot, buying your first home tends to happen concurrently with other costly endeavours: Getting married, going on a honeymoon, even planning for a baby.

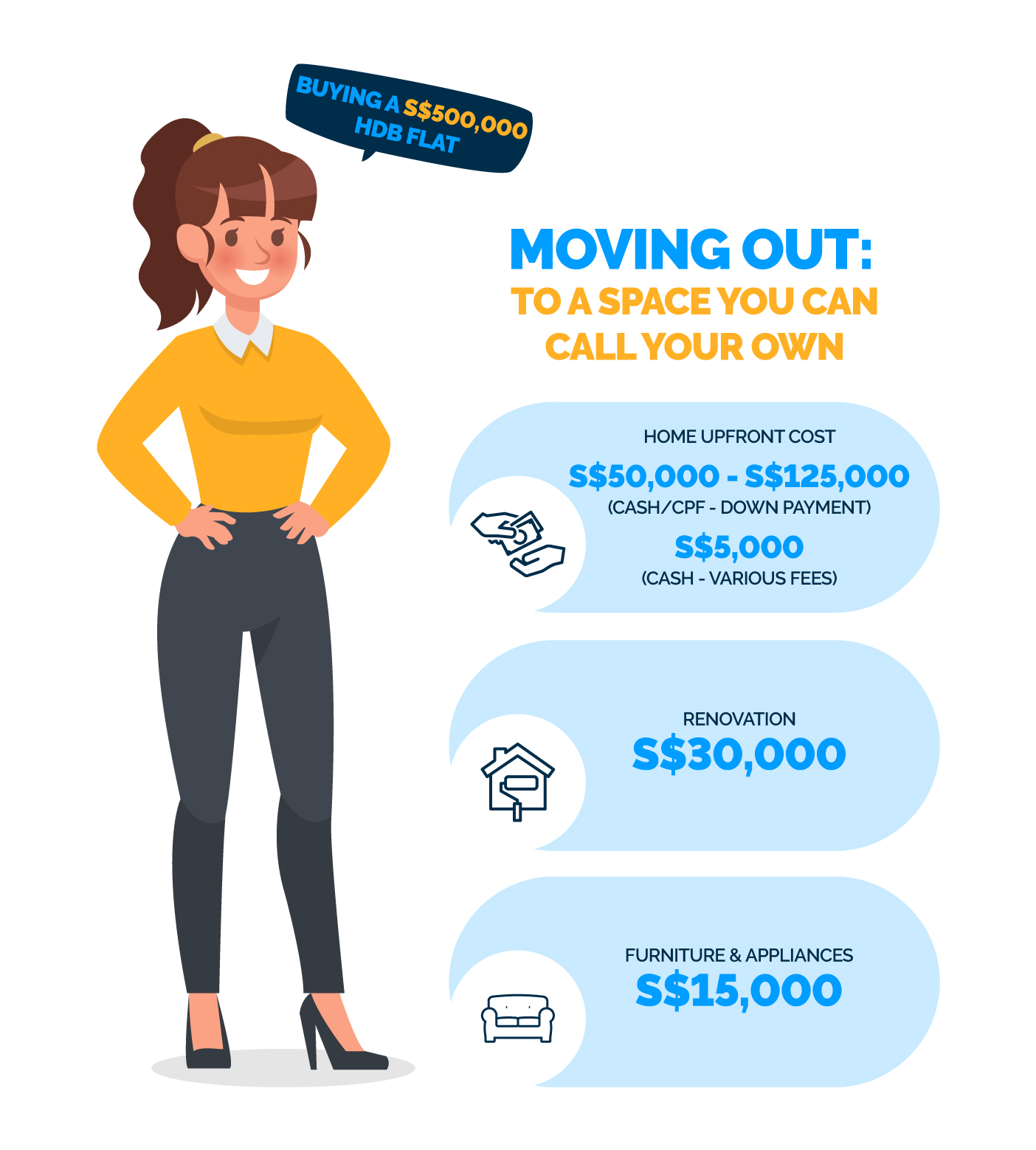

Once you get the keys, don’t forget that you’ll need to renovate your house, furnish it, and invest in electronics and appliances.

And for the first time in your life, you will have to pay for your own utilities, groceries, home maintenance, conservancy charges, property tax, home and fire insurance premiums… The list goes on.

Bear in mind that these costs are add-ons on top of your mortgage. So in your first few years of moving into your new home, you can expect:

Start Planning Now

Check out DBS MyHome to work out the sums and find a home that meets your budget and preferences. The best part – it cuts out the guesswork.

Alternatively, prepare yourself with an In-Principle Approval (IPA), so you have certainty on how much you could borrow for your home, allowing you to know your budget accurately.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?