A guide to how SRS accounts can work for you

No matter what stage you are in life, saving for retirement can seem like a daunting task. Sure, you have your Central Provident Fund (CPF) savings. But if you imagine what kind of lifestyle you picture yourself having post-retirement, you might start to wonder if it’s enough.

While your compulsory CPF savings can help you save for retirement, you can take a more proactive approach to saving more for your retirement with the voluntary Supplementary Retirement Scheme (SRS) which was introduced by the Singapore government in 2001.

On top of helping you save more for retirement, the SRS comes with a whole host of benefits that include tax reliefs. (Find out how much you can save with the SRS tax relief calculator). You can also use your SRS funds to invest and give your savings a boost through a wide range of instruments, ranging from the typical investment instruments to single premium insurance products.

How an SRS Account Works as a Retirement Planning Tool

You are eligible to sign up for an SRS account if you are a Singaporean, Permanent Resident (PR) or foreigner; at least 18 years old and not an undischarged bankrupt; have no existing or pending SRS account or account application with any bank; and can contribute varying amounts, subjected to a cap.

You can make an SRS contribution to top up your SRS account as many times a year as you like, up to a maximum of $15,300 for Singaporean citizens/PRs, and $35,700 for foreigners.

The SRS account can help you grow your retirement savings, so it is worth considering if you’ve reached the contribution limit on your CPF account. As mentioned earlier, it can also help you save on taxes - here’s how it works:

- You can reduce your final tax payable by getting a dollar-for-dollar tax relief on your SRS contributions which reduces your chargeable income.

- If you start withdrawing your SRS funds at the age of 63 you can get a substantial tax relief by only having to pay taxes on 50% of your withdrawals for the next 10 years.

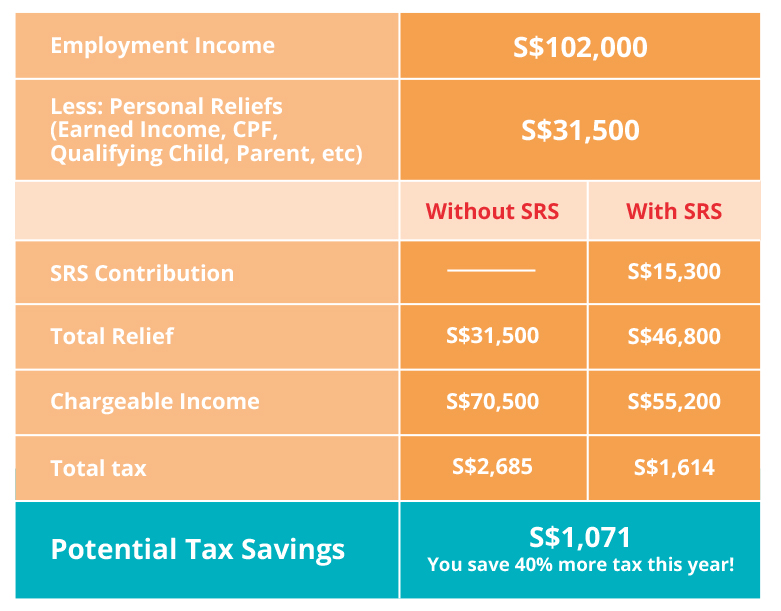

Need a play-by-play on the SRS tax relief? Here’s an example showing how SRS can help you reduce your chargeable income so that you can achieve significant tax savings:

How your SRS contributions can work even harder: Investing

Your SRS account is not just for retirement savings and tax savings, you can also use the money in your account to invest in a wide range of SRS-approved instruments like:

|

|

What’s more, whatever returns you make from your investments are credited directly to your SRS account where it can grow steadily, tax-free.

Unsure how to grow your SRS funds? Try the Invest your SRS Savings feature in DBS Plan & Invest tab in digibank to get personalised recommendations for your needs.

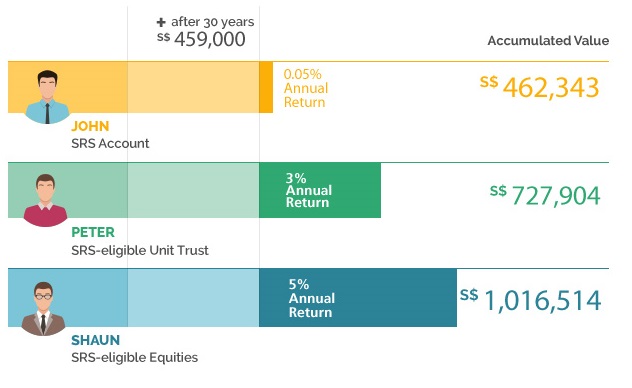

Here’s an example of how investment returns can help you to grow your SRS money. John, Peter and Shaun contribute $15,300 annually to their SRS accounts, giving them $459,000 in their respective accounts after 30 years of annual contribution.

But if you work investments in, as illustrated below, Peter and Shaun – who both invested a portion of their SRS accounts in SRS-approved instruments – will each accumulate more for their retirement than John who left his funds un-invested.

|

John is content to let his funds lie un-invested. This earns him an interest of 0.05% per annum (SRS deposit rate). |

|

Peter invests his funds in financial assets that earn him a return of 3% per annum. |

|

Shaun is slightly more aggressive when investing and he earns a return of 5% per annum. |

When can you withdraw from your SRS Account

Unlike CPF which has a strict minimum age for withdrawal of funds, you can withdraw your SRS monies anytime. Just note that if you withdraw before the current statutory retirement age of 63 years old, there will be a 5% penalty.

In addition, you can also withdraw the monies in two ways:

- Everything at one go

- Spread your withdrawals over 10 years

It’s not uncommon for SRS members to spread their withdrawals out over a longer period, and the government allows us 10 years to do so. This is known as the “10-year strategy”, and you can reap better tax benefits by maximising the 10-year grace period. The next section explains how.

The 10 Year Strategy

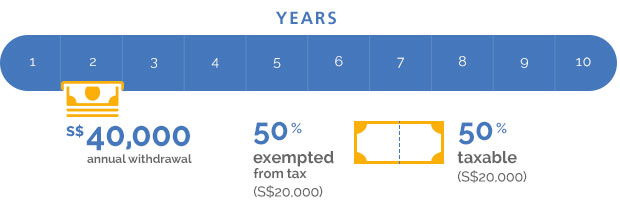

If you have accumulated $400,000 in your SRS account – the optimal amount of money to keep at retirement – you’ll be able to withdraw $40,000 each year for 10 years.

Keep in mind that during this 10-year window, only 50% of your withdrawals are taxable, which means that only $20,000 is subject to tax. Since the remaining $20,000 is exempted from tax, you have effectively reduced your tax payable, while setting up a steady income stream from your SRS account for 10 years.

If you have some SRS funds tied up in investments and prefer not to withdraw your them in cash, you can also apply to your SRS operator to withdraw an SRS investment by transferring it out of your SRS account (e.g. into your personal Central Depository (CDP) account), without having to liquidate your SRS investments. Terms and conditions apply.

It’s not uncommon to wonder if you’re really saving enough for your future, but with effective planning and a good strategy, Singapore's SRS can certainly help you increase your retirement funds.

Ready to start?

Get started with SRS. If you do not have an SRS account, open* one instantly via digibank.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Tell us if this article helps you plan and achieve your financial goals

![]()

![]()

![]()

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

* Income tax savings based on the assumption that a married male Singapore Citizen has an annual income of $102,000 in 2015 and enjoys total personal tax relief of $31,500 (Earned Income Relief of $1,000, CPF Relief of $17,000, NSman Self Relief of $5,000, Qualifying Child Relief of $4,000 and Parent Relief of $4,500) and SRS relief of $15,300 for the Year of Assessment 2016.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?